Even with the current interventions in place to freeze consumer energy prices (referring here to electricity and gas), millions of households are experiencing fuel poverty this winter. [1] Now extended until April 2024, the price guarantee — while welcome to stave off an acute crisis with potentially devastating impacts — offers a direct support for energy retail companies, using public money to cover the difference between the actual wholesale energy price and an agreed limit price. Critically, it does not represent a long-term solution for structural deficits in how Britain’s energy system is owned and organised. Resolving the crisis facing households and businesses while preventing similar upheavals from occurring in the future requires us to fix these deficits. Doing so means a fundamental rethink of how our energy system is organised. While energy is often used to refer to both electricity and gas used for heating, in this Explainer we focus specifically on electricity.

Multiple factors have driven spiralling energy prices over recent months, most critically Russia’s invasion of Ukraine and its impacts on gas supply and prices. [2] However, long before these acute pressures, the privatised and market-based organisation of Britain’s [3] energy system left us uniquely exposed to such shocks, with the result that the UK has been the worst hit of any western European country by the crisis rocking global gas prices. [4]

We need an energy system that is secure, green, and affordable for all. Delivering it means rethinking the current system, including the privatised, market-based, and for-profit logics that organise it. In this explainer, we explore the design of Britain’s existing electricity system. In subsequent papers we will set out a range of alternatives and policy solutions that can reimagine it for the long term.

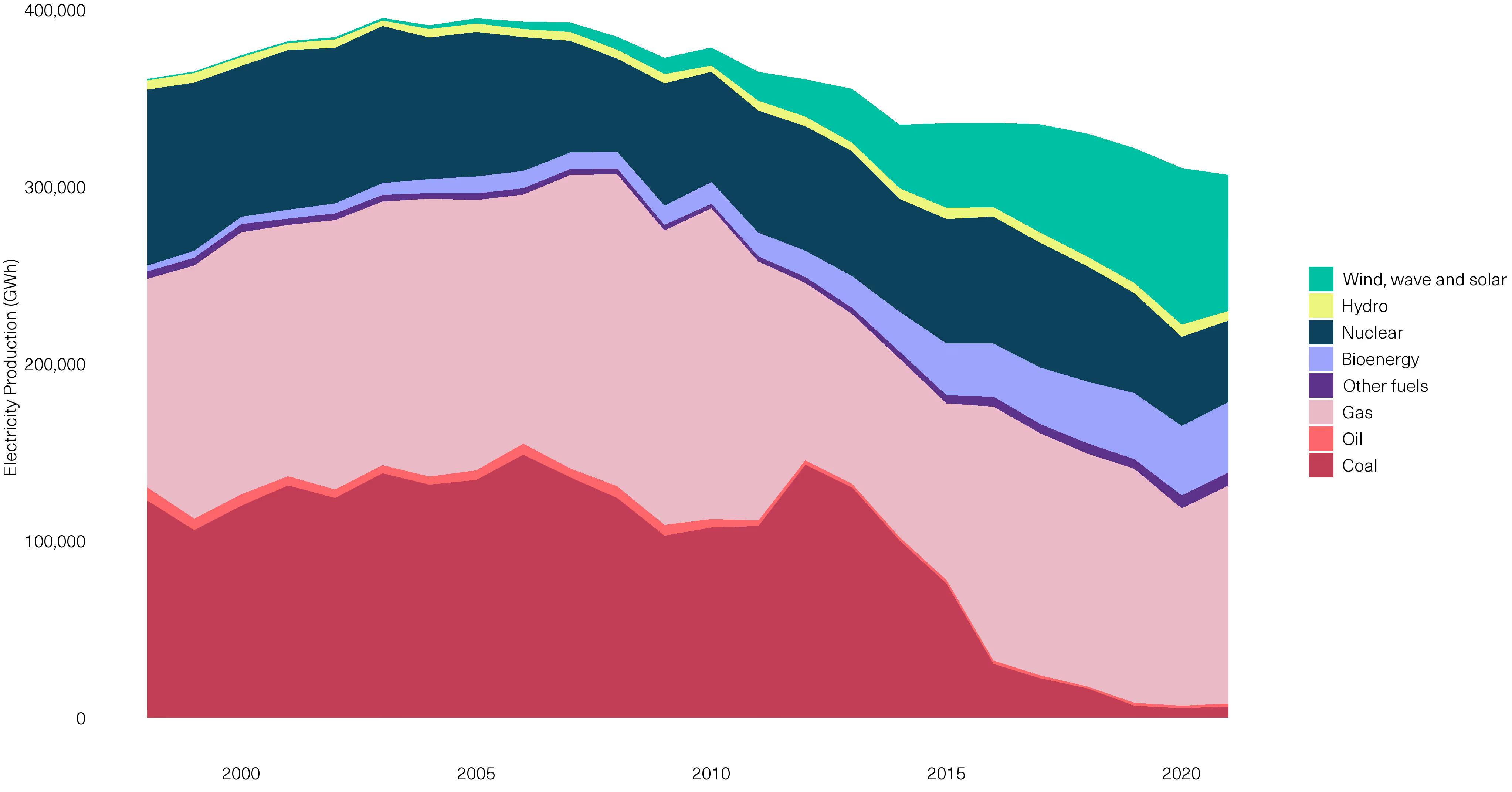

Britain is unusual in having an almost entirely privatised electricity system, including a privately owned energy grid. [5] The sequence of steps that delivers electricity from producers to households is outlined in Figure 2 below. The path in Figure 2 specifically follows the journey of gas-powered electricity, which accounts for approximately 40% of UK electricity generation [6] (see Figure 1) — making Italy the only European country more reliant on gas than the UK. [7]

[.img-caption][.img-caption-header]Figure 1 UK Electricity Production by Source[.img-caption-header][.img-caption-text]Source: BEIS Digest of UK Energy Statistics (DUKES)[.img-caption-text][.img-caption]

As Figure 1 above shows, Britain’s electricity is derived from several sources; however, given its principal role in British electricity supply today and its centrality to the energy bills crisis, we focus on gas for the purposes of this briefing. For other sources such as nuclear and renewables, much of the journey is equivalent, though details related to resource extraction are, of course, unique to different energy sources.

[.img-caption][.img-caption-header]Figure 2 The Journey of Gas Powered Electricity[.img-caption-header][.img-caption]

For gas-powered electricity, the first step is the extraction and processing of fossil gas for use in electricity generation. Some companies involved in this process are household names, like Shell and BP, but there are thousands of smaller companies involved in the global system of oil and gas extraction and processing (hereafter simply termed “production”). Our research found over 120 different companies with equity stakes just in the UK’s North Sea oil and gas assets. [8]

In 2021, Britain’s domestic gas demand was 23.3 billion cubic meters (bcm, the unit of volume for fossil gas), of which approximately 8 bcm was used for electricity generation (both household and other uses). [9]

By comparison, gas production from the North Sea in 2021 was approximately 90 million cubic meters per day — equivalent to nearly 33 billion cubic meters per year [10] and importantly, more than total domestic demand. [11] However, just under half of the gas extracted from the UK Continental Shelf in the North Sea (15.6 bcm) tends to be allocated for domestic use, [12] with much of the remainder exported on the global market.

In the midst of the energy crisis, despite a significant ramping up of gas production in the North Sea, the UK’s gas exports have reached record highs, with exports in April–June (Q2) of 2022 a remarkable 576% higher than the same period in 2021. [13] This explosion in exports at a time of a crisis in domestic supply and cost is the product of the market-based approach to fossil fuel production in the UK, whereby the companies extracting and producing this gas simply sell it for the highest price they can achieve on the global market — in this case, for export via pipelines to Belgium and the Netherlands, rather than to meet domestic energy needs. [14]

Before it can be used for electricity, extracted gas must be processed. This may be done by the same firms that extracted it or by specialist processing companies. For instance, specialist asset management company px Group owns several processing plants responsible for 30% of the UK’s gas supply, [15] while an additional third of UK supply is processed at the Bacton Gas Plant in Great Yarmouth, owned by Shell. [16]

Once gas is processed, it is sold to one of the 16 different electricity-generating firms who own and operate one or more of the 45 fossil gas-fired power plants currently operational in the UK (shown in Figure Three). [17] Many of these plants are owned by major international energy firms, such as Germany’s RWE and the French state-owned EDF. Some generating companies, like Centrica, have businesses at every stage of the energy system, including extraction, generation and supply. This vertical integration in part enabled Centrica (the parent company of British Gas) to report an adjusted profit of £1.34 billion in July 2022, up from £262 million a year earlier. Following this spike in profits - related directly to surging global gas prices and, by extension, energy bills - Centrica resumed dividend payments for the first time since the pandemic started, totalling £59 million. [18]

[#map][.img-caption]Figure 3 Who Owns the UK’s Gas Power Stations?[.img-caption][#map]

[.box][.box-header]Box One: What is the Wholesale Market?[.box-header][.box-paragraph]The price per unit of electricity in Britain is set by the “wholesale market”, where companies generating electricity sell power to traders and suppliers. Importantly, the market functions in a way that means the price per unit is largely set by the cost of gas power generation.[.box-paragraph][.box-header2]How Does It Work?[.box-header2][.box-paragraph2]Britain uses a marginal pricing system. Every half hour, the wholesale price of electricity is determined by the “marginal generation unit”, which refers to the source for the last unit of electricity required to meet demand. When organising power to meet demand, electricity sources follow a “merit order”. The cheapest sources, including renewables and nuclear, get deployed first. Gas is among the more expensive sources of electricity generation, but still provides approximately 40% of domestic electricity; as a result, it generally tends to provide the marginal unit after other sources, namely nuclear and renewables, are deployed, thereby setting the price per unit for all sources. In this way, the price of all electricity in Britain is broadly pegged to the price of gas. In our next paper, we explore alternative designs for a wholesale market fit for a green energy future.[.box-paragraph2][.box]

Once electricity is generated from the gas-fired plants, it is sold on the “wholesale market” (explained in more detail in Box One) to electricity suppliers, the consumer-facing firms that provide tariffs to households and businesses (see Steps Three and Four below). These include the “Big Five” (British Gas, E.ON, EDF, ScottishPower and OVO), as well as many smaller suppliers.

Suppliers purchase electricity directly from generators and traders in the wholesale market. However, neither suppliers nor generators control the infrastructure needed to physically deliver electricity from generators to end-users. Instead, this infrastructure is broken up into two separate components. The first is long-range transmission. The infrastructure for this step is wholly owned and operated by National Grid plc and its affiliated and subsidiary companies. The second component involves more localised networks that connect directly to households and businesses, either from the National Grid or, in some instances, from local energy producers. These networks are owned and operated by a set of companies called Distribution Network Operators (DNOs). Both the National Grid and DNOs charge suppliers (the retail companies from which households buy their energy) for the use of their infrastructure, who pass that cost — alongside the wholesale cost of electricity and a handful of other costs — on to end users like households and businesses. These “network costs”, which average roughly 20% of a household’s bill, largely reflect use of transmission and distribution infrastructure, but also include charges for “balancing” — the supply and demand coordination carried out by National Grid’s Electricity System Operator (a separate but related company to National Grid plc), and can also include levies for exceptional circumstances, such as suppliers going bust. Recent estimates place the energy network charges at roughly £370 for the average annual household bill. [19]

Importantly, both transmission and distribution networks are “natural monopolies”, meaning there are either structural limits to the ability to create competition in these sectors, or clear reasons for not doing so. In the case of large infrastructural networks used in transmission and distribution, it makes little sense with respect to efficiency or practicality to have multiple networks of cables performing the same function. [20] As a result of this monopoly arrangement, the DNOs have been able to maintain exceptionally high profit margins for several years. [21] Indeed, according to National Grid, while charges for use of the long-range grid infrastructure constitute approximately 3% of an average household bill, these “other networks” account for closer to 20%. [22]

Energy suppliers, including the Big Five and several smaller competitors, set tariffs for electricity usage with households and businesses. These tariffs reflect various costs at all the preceding steps in the chain, from production to the wholesale market to distribution, with prices at every stage set high enough to ensure firms can turn comfortable profits and, in many cases, pay out substantial sums to shareholders (see Problem Two below). The rates charged by suppliers are regulated by Ofgem via the “price cap”, a market-regulating mechanism that has been at the centre of debate throughout the current energy bills crisis. The supply sector is meant to be a competitive market that allows households and businesses to shop around for the best deal. However, although there are several smaller energy competitors, the supply market remains highly concentrated, with the top nine suppliers alone controlling 77% of market share as of 2020, the most recent available estimate (though down from a high of 97% in 2010). [23]

The price cap, which regulates the extent to which suppliers can mark up the cost of electricity via Ofgem, has been the subject of intense scrutiny and debate throughout the course of the present crisis in energy bills, with many confused or frustrated at the cap’s apparent inability to keep prices affordable for households and businesses. Critically, however, the purpose of the price cap for electricity is not to keep prices low overall, raising the question: what is the price cap for?

In contrast to the idealised image of a smooth, efficient and competitive market often invoked to defend privatisation, the British energy market is defined by very poor rates of consumer switching and “shopping around” for the best deal, indicating low competitiveness. In Ofgem’s own words, “[c]ustomers who don’t shop around and get stuck on their supplier’s basic default energy tariff are disadvantaged in the energy market.” [24] The price cap was thus implemented to prevent suppliers from taking advantage of consumers on default tariffs under these conditions of low consumer switching. In other words, one might argue Ofgem’s price cap is premised on a recognition that competitive conditions — whereby firms’ behaviour is disciplined by consumer fickleness — do not exist in this market, and hard regulatory barriers are needed to prevent exploitation of consumers that might otherwise ensue. This, rather than lower overall prices per se, is the rationale for the price cap.

With this purpose in mind, it becomes easier to understand why the price cap has consistently risen during this crisis to ensure regulated companies can continue to be profitable and, by extension, viable. Thus, the design of the cap means that even extraordinary profits captured further up the supply chain, such as those of fossil fuel producers in recent months, [25] and which are embedded into the suppliers’ input costs, are not considered relevant to the consumer-supplier relationship that the price cap is designed to regulate. As a consequence, the surge in gas prices this year have been transmitted directly through to household bills.

As noted at the start of this Explainer, there are multiple short-term factors currently driving soaring electricity prices, most acutely the conflict in Ukraine and its impact on the global gas market, with prices rising 250% between January and the end of September 2022. [26] However, long before that crisis began, Britain’s energy system had been reorganised through the process of privatisation around the interests of private firms, their shareholders, and commodity traders, rather than long-term energy security and affordability. By keeping Britain highly reliant on gas generation; leaking billions to shareholders; and broadly pegging the price of all electricity to the price of gas, the scale of the current energy crisis has been exacerbated by the privatised and market-based organisation of electricity provision. Absent a transformation in this system, we leave ourselves exposed to the risk of similar shocks — and further pain for households and businesses — particularly in the context of a worsening climate crisis.

Below, we look briefly at three key issues, which will be examined in depth in subsequent briefings and reports over the coming months.

One of the critical issues with the existing system, made particularly clear by the current explosion in energy bills, is the design of the wholesale market, which a government review into electricity market reform explicitly states was “designed for a fossil fuel-based electricity system." [27] The same review warns of a “growing mismatch” between the design of the wholesale market and a green energy future. [28]

The wholesale market pricing mechanism has played a major role in transmitting shocks like the conflict in Ukraine directly onto families in the Britain by linking the cost of electricity to gas. In other words, because of this price linking (see Box One), electricity bills as a whole have surged, even though other sources like renewables remain cheap, with very low generating costs. The need for reform is clear.

The government has opened a review into the wholesale market. In our next publication on the energy crisis, we will provide an in-depth review of available policy proposals for wholesale market reform. The key task will be to ensure a newly designed system prioritises the needs of people and planet rather than, as the next section lays out, private companies’ profits.

When we look at the operation of the energy system as a whole, one key trend is clear: privatisation along every link in the chain outlined in Figure 2 has served as a highly effective mechanism for generating high profits for private companies and distributing cash to shareholders.

At the upstream end of the energy chain, soaring global gas prices have meant that Shell and BP posted exceptional profits over the four quarters from October 2021 to September 2022 of a combined $81 billion, with $36 billion paid out to shareholders in the form of dividends and buybacks. [29] Latest figures suggest the world’s top five oil majors will post combined profits of $190 billion for 2022. [30]

However, fossil fuel extraction is not the only area of the energy system in which massive payouts have been made to shareholders over recent years. For example, as our recent briefing outlines, in the five years between March 2018 and March 2022, National Grid plc (which has operations in both Britain and the US) paid out £8.9 billion to shareholders in dividends and buybacks. [31] The DNOs, meanwhile, enjoyed the highest profit margins of any sector of the UK economy in 2021, at 42.5%.[32] These exceptional margins are not a fluke event; they have been consistent over much of the past decade. A 2017 report by the Energy and Climate Intelligence Unit concluded that from 2010-2015, the average profit margin posted by the DNOs was “huge by any standard” at 32%, adding a total of £10 billion to the national energy bill over the same period. [33] And, according to reporting by the Financial Times, UK Power Networks, which services London, the Southeast and East Anglia and is owned by Hong Kong billionaire Li Ka-Shing through CK Infrastructure Holdings, “paid a £217 million dividend to its owner in the year to 2022”, having posted a pre-tax profit of over £530 million. [34]

While operating profit margins are only one measure of profitability, and do not, for instance, reflect capital employed, the essential concern in a vital industry like household energy provision should be universal affordable access, and these exceptional margins suggest a considerable portion of income and expenditure flows are being cashed out as profits (for further explanation, see our recent briefing). Indeed, in its 2019 State of the Energy Market Report (the most recent available), Ofgem admitted the “overall costs of the transmission and distribution networks to consumers … have turned out to be higher than they needed to be. In practice, the majority of network companies are achieving profit margins towards the higher end of our expectations for each sector.” [35] These conclusions raise clear doubts over how the delivery of a vital service we all need to survive and thrive by private, for-profit monopolies, can continue to be justified.

The major electricity suppliers have also made large shareholder pay-outs over the past several years. Common Wealth research found that in the five years between 2016 and 2020, the Big Six suppliers (now the Big Five, following the acquisition of SSE by OVO and the merging of the customer bases of npower and E.ON) paid out the equivalent of 82% of their pre-tax profits in dividends. [36]

In response to criticism of large shareholder payouts, the argument is commonly made that dividend income pays our pensions, and that making efforts to reduce them is therefore tantamount to attacking the income security of pensioners. However, recent analysis by the TUC, Common Wealth and the High Pay Centre found that this is far from representative of reality. In practice, UK pensions own just 6% of UK corporate shares, whether directly or indirectly (i.e. via an intermediary investment management firm). [37] Moreover, UK pension funds typically allocate only a portion of their assets (less than 20% on average) to equities, of which UK equities are only one fraction. [38] When combined with the highly unequal distribution of pension assets relative to income bracket and the shift over time to “defined contribution” pensions, the benefit of these dividend payments is minimal, with what little income these dividends may offer skewed towards the highest-income pension holders.

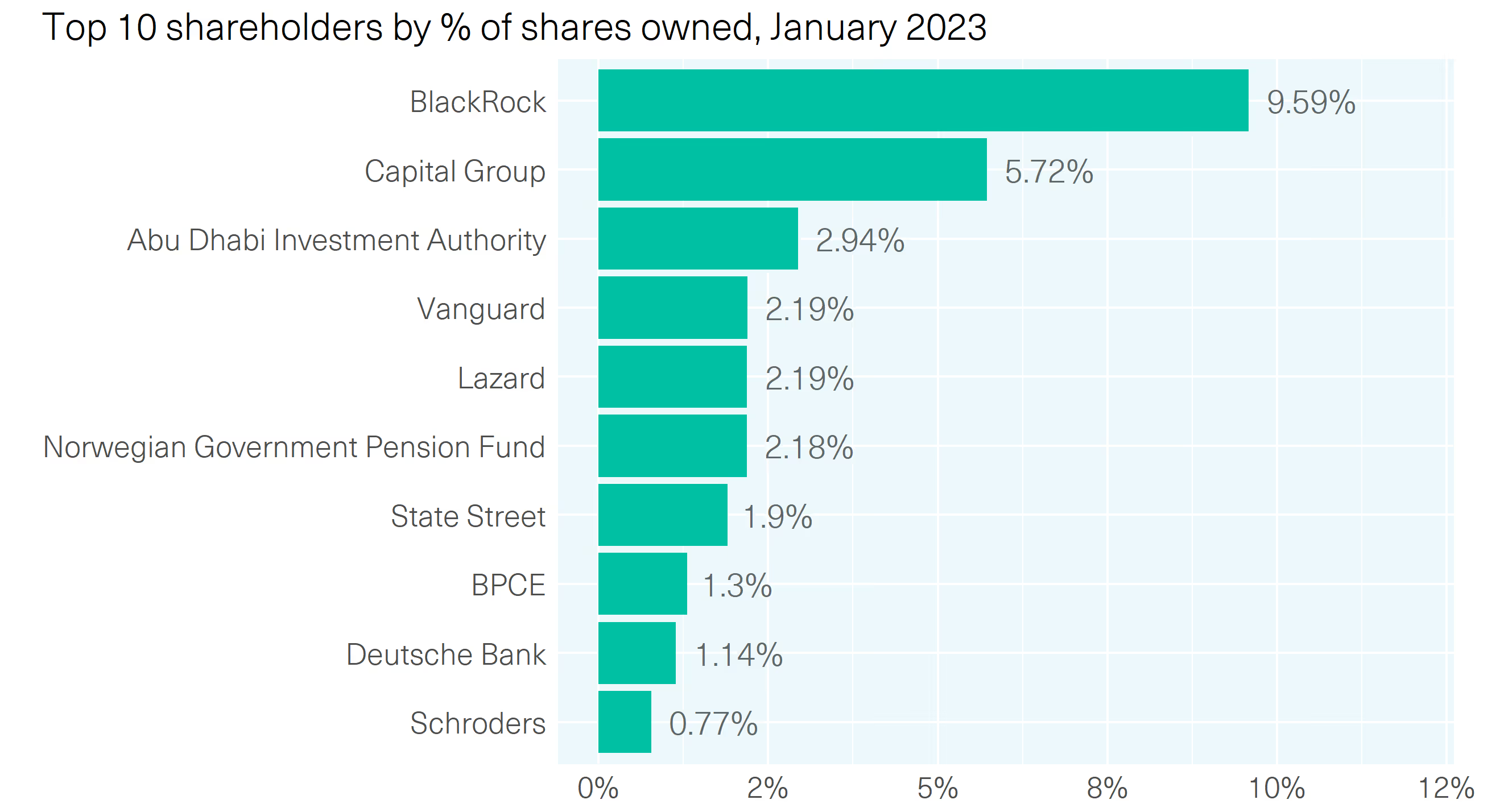

In practice, ownership of the UK’s publicly listed energy firms is highly internationalised, meaning the profits and payouts from our energy bills are being distributed around a network of global shareholders, with ownership skewed toward the asset-rich and often including other government authorities, from the Norwegian sovereign wealth fund to the Abu Dhabi Investment Authority, the fourth largest shareholder in National Grid (Figure 4).

[.img-caption][.img-caption-header]Figure 4 Who Owns National Grid?[.img-caption-header][.img-caption-text]Source: Common Wealth analysis of Refinitiv database[.img-caption-text][.img-caption]

While raising revenue for government was an early argument used to justify privatisation, today the continuation of this system is often defended on assumptions about market mechanisms, such as the premise that market-based provision improves efficiency through competition, or that private ownership and provision allows private capital to be leveraged for investment, saving public money.

In light of the current state of Britain’s energy system, it is worth examining these premises to determine whether they hold up. While Britain has managed to deliver impressive growth in renewable energy generation over the past decade (see Figure 1), government policies, incentives and supports have been critical to the speed and scale of this transition, including the Renewables Obligation, [39] feed-in-tariffs for small-scale renewable installations, [40] and the more recent “Contracts for Difference” mechanism, which guarantees certain prices for renewable energy generators to encourage investment in new low-carbon energy generation. [41]

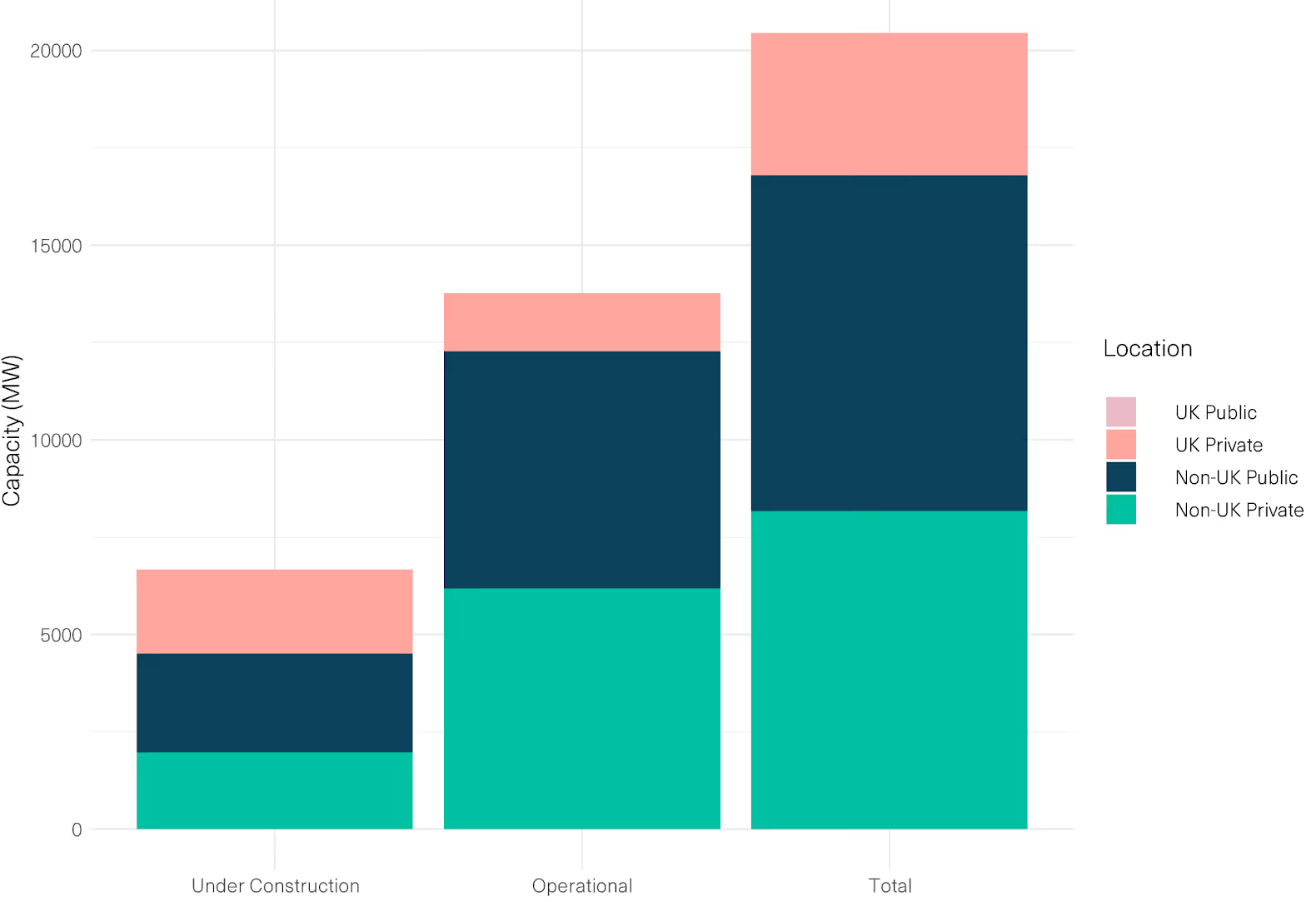

According to research from the World Economic Forum, nine of the ten countries leading the global transition to renewable energy have a publicly-owned renewable generation company, from Norway’s Statkraft to EDF in France — with the UK being the only top ten country that does not. [42] As Common Wealth’s recent research found, over 40% of the UK’s offshore wind capacity is publicly owned — just not by the UK public. Instead, it is owned by foreign governments, with the UK public owning just a tiny 0.03% share — less than the government of Malaysia. [43] As the same report argues, a publicly-owned renewable energy champion could accelerate the transition to 100% clean energy with strategic public investment, while sidestepping the wholesale market with power purchase agreements; in doing so, it could grow public wealth while cutting energy bills by eliminating our reliance on volatile fossil gas. [44]

[.img-caption][.img-caption-header]Figure 5 Ownership of UK Offshore Wind Capacity[.img-caption-header][.img-caption-text]Source: Common Wealth analysis based on ownership data from the Crown Estate’s 2021 Offshore Wind Report; capacity data from 4C database; and capacity factor data from energynumbers.info[.img-caption-text][.img-caption]

However, even with a public generator, a major issue facing further urgent roll out of renewables is connection to the National Grid and regional distribution networks. As a report this year by the Financial Times noted, renewable generators currently face between a six and ten year wait before they can be connected to the grid due to inadequate investment and planning on the part of the transmission and distribution network companies. [45]

Ofgem regulates the maintenance expenditure and capital investment budget of the transmission and distribution networks by establishing agreed targets; however, expert analyses have suggested these may often be inadequate or unmet. [46] Insufficient investment in maintenance has been linked to several blackouts and grid issues in recent years. [47] Critically, as demand continues to rise, the pressure placed on aging networks is increasing their tendency to “leak”, resulting in a loss of roughly 25 terawatt hours in 2022 — equivalent to the total quantity of energy imported to the UK this year. [48]

In November, National Grid committed to investing £40 billion over the next four years in grid infrastructure. [49] The commitment comes alongside Ofgem’s announcement of a long-term plan for major investment in upgrading the UK’s power networks. Importantly, Ofgem concedes that “[t]he costs of the electricity distribution grids are ultimately paid for by consumers who are currently facing extraordinary pressure on their household bills,” and so have committed to significantly reducing network operators’ permitted rates of return to ensure “less of consumers’ money goes to company profits.” [50]

The question remains as to why, under monopoly conditions and with a consumer base who cannot choose not to access electricity, company profits are justified at any level. Indeed, high profits and payouts in the case of Britain’s network operators are indicative of excess energy costs for households and businesses, rather than the “success” of a competitive business. Further, with average borrowing costs for private companies higher than those for the public sector, the buildout and maintenance of a modernised grid could be achieved more cost efficiently through public investment. These questions will be explored in further depth in future reports.

Britain’s energy system has been buckling this winter, exposing weaknesses rooted in the logics that private, for-profit ownership impart to the design and operation of the system. Though external shocks have put immense pressure on that system, its underlying structures have left us more vulnerable and intensified the cost of this crisis. Addressing these issues durably will therefore require deep reform, rather than limiting policy ambition to expensive short-term sticking plasters.

There are many areas within Britain’s electricity system where policymakers could intervene to improve outcomes for households, businesses and the planet. The core goal of any such intervention should be to break with our current status quo: the unsustainable extraction of fossil fuel resources from the planet and of wealth from ordinary people.

Achieving this implies a shift in paradigm from a private and profit-driven electricity system built around the interests of fossil capital, to a public system that is governed and operated according to social and climate needs. While there are multiple policy pathways that could be pursued toward that end, what is clear is that we need an ambitious plan to: drive investment in the infrastructure required to decarbonise our grid; rapidly scale up renewable generation and “flexible” low-carbon options; reduce or altogether eliminate shareholder payouts; and ultimately to guarantee secure, affordable, green electricity for all. Those goals are best secured if we shift from a system of private financing, ownership and governance, and profit-focused goals to an energy future based on public investment and public ownership, non-financial governance, and social and environmental priorities.

From creating a new renewable energy generator champion to guide the transition, to ensuring transmission and distribution networks are back in democratic public ownership, to a public supplier that can operate outside of a wholesale market pricing system no longer fit for purpose — ambitious reform is the surest route to resolving the energy crisis. We will set out pathways to doing so in upcoming research, to be published over the first half of 2023.

[#fn1][1][#fn1] “Energy Crisis”, National Energy Action, October 2022. Available here.

[#fn2][2][#fn2] Susanna Twidale, “Explainer: Why Russia drives European and British gas prices”, Reuters, 02/09/22. Available here.

[#fn3][3][#fn3] Northern Ireland has a separate electricity market and regulator from Great Britain. We refer here to the system in place in England, Scotland and Wales. For further explanation, see here.

[#fn4][4][#fn4] Damian Carrington, “Energy Crisis: UK Households Worst Hit in Western Europe, finds IMF”, The Guardian, 01/09/22. Available here.

[#fn5][5][#fn5] Vera Weghmann, “Going Public: A Decarbonised, Affordable and Democratic Energy System for Europe”, PSIRU University of Greenwich, 07/22.

[#fn6][6][#fn6] The fraction of electricity generated from gas varies in real time depending on several factors, including e.g. wind and sun conditions on a given day. This figure represents a long-running average, via “Analysis: Why UK energy bills are soaring to record highs – and how to cut them”, Carbon Brief, 12/08/22. Available here.

[#fn7][7][#fn7] Carrington, “Energy Crisis”, The Guardian. Available here.

[#fn8][8][#fn8] “Who Owns the North Sea: Interactive Map”, Common Wealth. Available here.

[#fn9][9][#fn9] “Gas Summer Outlook Report April 2020”, National Grid, 2021. Available here.

[#fn10][10][#fn10] Laura Hurts and Elena Mazneva, “UK Gas Production Brings Some Respite in Mounting Energy Crisis”, Bloomberg, 25/08/2022. Available here.

[#fn11][11][#fn11] “Gas Summer Outlook”, National Grid. Available here.

[#fn12][12][#fn12] Ibid.

[#fn13][13][#fn13] “Energy Trends UK, April to June 2022”, Department for Business, Energy and Industrial Strategy, September 2022. Available here.

[#fn14][14][#fn14] Ibid.

[#fn15][15][#fn15] See here.

[#fn16][16][#fn16] “About Bacton Gas Plant”, Royal Dutch Shell. Available here.

[#fn17][17][#fn17] The full list of the owners/operators of the UK’s gas-fired power plants can be found in Figure 3, derived from “DUKES (Digest of UK Energy Statistics): electricity”, Department for Business Energy and Industrial Strategy, 28 July 2022. Available here.

[#fn18][18][#fn18] David Sheppard, “Centrica reinstates dividend as profits soar during energy crisis”, The Financial Times, 28/07/22. Available here.

[#fn19][19][#fn19] Gill Plimmer, “UK electricity monopolies under scrutiny over network investment”, The Financial Times, 30/08/22. Available here. Jillian Ambrose, “How the UK energy price cap is calculated – and how it affects your bill”, The Guardian, 03/02/22. Available here.

[#fn20][20][#fn20] Monopoly Money: How the UK’s electricity distribution network operators are posting big profits”, Energy and Climate Intelligence Unit, September 2017 Available here.

[#fn21][21][#fn21]bid; Joseph Baines and Sandy Brian Hager, “Profiting Amid the Energy Crisis: The Distribution Networks at the Heart of the UK’s Gas and Electricity System”, Common Wealth, 14/03/22. Available here.

[#fn22][22][#fn22] Note: these figures may be slightly out of date, as they reflect average 2021/22 conditions. Source: “Breaking down your electricity bill”, National Grid. Available here.

[#fn23][23][#fn23] Addy Mettrick, “Competition in UK electricity markets”, Department for Business, Energy and Industrial Strategy, 30/09/21. Available here.

[#fn24][24][#fn24] “Energy Price Cap Explained”, Ofgem. Available here.

[#fn25][25][#fn25] Sam Meredith, “Big Oil poised to smash annual profit records — sparking outcry from campaigners and activists”, CNBC, 27/01/23. Available here.

[#fn26][26][#fn26] Hamish Penman, “Stark figures show North Sea gas production could be on course to wrap up by 2030”, Energy Voice, 23/09/21. Available here.

[#fn27][27][#fn27] “Review of Electricity Market Arrangements: Consultation Document”, Department for Business, Energy and Industrial Strategy, July 2022. Available here.

[#fn28][28][#fn28] Ibid.

[#fn29][29][#fn29] Adjusted profit metrics are used to adjust for exceptional items such as, for example, BP’s disposal of its stake in Rosneft in Q1 2022. For BP we use “underlying replacement cost profit”, and for Shell, “earnings on a CCS basis excluding identified items”.

[#fn30][30][#fn30] Meredith, “Big Oil poised”, CNBC. Available here.

[#fn31][31][#fn31] Common Wealth analysis of corporate filings and Refinitiv financial database.

[#fn32][32][#fn32] Sandy Brian Hager and Joseph Baines, “Profiting Amid the Energy Crisis: The Distribution Networks at the Heart of the UK’s Gas and Electricity System”, 2022, Common Wealth. Available here.

[#fn33][33][#fn33] “Monopoly Money: How the UK’s electricity distribution network operators are posting big profits”, Energy and Climate Intelligence Unit, September 2017. Available here.

[#fn34][34][#fn34] Plimmer, “UK electricity monopolies under scrutiny over network investment”, The Financial Times. Available here.

[#fn35][35][#fn35] "State of the Energy Market”, Ofgem, 03/10/19. Available here.

[#fn36][36][#fn36] Sandy Brian Hager, Joseph Baines and Miriam Brett, “Power Ahead: An energy system fit for the future”, 21/10/21, Common Wealth. Available here.

[#fn37][37][#fn37] “Do Dividends Pay Our Pensions?”, The TUC, Common Wealth and the High Pay Centre, 10/01/22. Available here.

[#fn38][38][#fn38] Harriet Agnew, Josephine Cumbo and Jonathan Eley, “Pension funds after the gilts crisis: the big asset allocation rethink”, The Financial Times,08/11/22. Available here.

[#fn39][39][#fn39] The Renewables Obligation requires suppliers to purchase a growing share of their electricity in the form of “Renewables Obligation Certificates”, either from qualified generators or from their own renewable power generation. For further detail see Marco Dell’Aquila et al., “The Role of Policy Design and Market Forces to Achieve an Effective Energy Transition: A Comparative Analysis Between the UK and Chinese Models” in The Geopolitics of the Global Energy Transition, 10/06/20. Available here.

[#fn40][40][#fn40] These contracts secured long-term, guaranteed prices for small-scale renewable producers, encouraging investment.

[#fn41][41][#fn41] “How the UK transformed its electricity supply in just a decade”, Carbon Brief, 2019. Available here. “Contracts for Difference”, Department for Business, Energy and Industrial Strategy, 13/05/22. Available here.

[#fn42][42][#fn42] “Fostering Effective Energy Transition: 2021 Report”, The World Economic Forum, 04/21. Available here.

[#fn43][43][#fn43] Mathew Lawrence, “Power to the People: The Case for a Publicly Owned Generation Company”, Common Wealth, 26/9/22. Available here.

[#fn44][44][#fn44] Ibid.

[#fn45][45][#fn45] Gill Plimmer, “Renewables projects face 10-year wait to connect to electricity grid”, The Financial Times, 08/05/22. Available here.

[#fn46][46][#fn46] Ian Brown, “Why the National Grid blackout is indicative of underinvestment in the future of the UK electricity market”, Arrowpoint Advisory, 09/09/19. Available here.

[#fn47][47][#fn47] Ibid.

[#fn48][48][#fn48] Ibid.

[#fn49][49][#fn49]Nicholas Earl and Ilaria Grasso Macola, “National Gird urges ‘transparency’ as it commits £40 bn to UK’s energy system”, City AM, 10/11/22. Available here.

[#fn50][50][#fn50] “Ofgem reveals landmark five-year programme to deliver reliable, sustainable energy at the lowest cost to consumers”, Ofgem, 29/06/22. Available here.