Great British Energy (GB Energy) stands as Labour’s most ambitious climate policy and a central mechanism to deliver decarbonisation and reverse national decline in government. As GB Energy is being rapidly designed and established as a matter of priority for the new Labour Government, an immediate concern is how this ambitious, nascent institution will translate low carbon generation into genuinely lower bills for consumers, both as an end in itself and as the means for building a coalition of deep support for the policy. According to YouGov polling commissioned by Common Wealth, the public already have high expectations that GB Energy will decrease their bills, with 36 per cent of the public and, notably, 53 per cent of Labour voters believing this will happen over the next five years.

To achieve this, alongside owning and operating renewable generation assets, GB Energy should include a consumer-facing supply arm to help overcome inefficiencies and redundancies in the retail and wholesale electricity markets. A "public option" retail arm of GB Energy would open up a progressive policy space to translate low-cost clean energy generation into durably lower bills.

[.box][.box-paragraph]A public option energy supplier would be a fully publicly-owned retail energy company that households and businesses can choose to buy electricity from. Recent polling suggests that 45 per cent of the public would want to see GB Energy be a state-owned company that they can purchase energy from to supply their home.[1] As GB Energy need not pay dividends to private investors — unlike the “big six” (the six largest energy companies operating in the UK) who paid £23 billion in dividends between 2011 and 2020[2] — the public option could more fully pass on costs savings of cheap renewable power and more equitably distribute the costs of building new capacity across consumers.[.box-paragraph][.box-paragraph]The strategic objectives and purpose of the public option would be defined by the Government, but day to day decisions about hedging, tariff design and customer service should be made independently.[.box-paragraph][.box-paragraph]The term "public option" originates in the United States healthcare policy debate where it refers to proposals for the government to set up a health insurance scheme that would compete with private insurers. We use the term here deliberately as we think the British energy retail market has parallels with the extractive and socially damaging US private healthcare system.[.box-paragraph][.box]

This note argues that a GB Energy branded public option for retail electricity will provide a powerful lever to bring coherence to the current path of electricity system restructuring that is already occurring, and allow for progressive price policies and a gradual decommodification of electricity. Creating a public option retail arm would also position the GB Energy brand directly towards households and businesses. If well delivered, this could help to build a broad-based coalition of support for GB Energy and wider public action to address the interconnected climate and cost of living crises. This briefing argues that:

The retail market involves licensed suppliers selling electricity to final consumers that they have in turn purchased from generators through the wholesale market. The retail market can thus be thought of as the interface between the original generators of power and the final consumers of power. An explainer previously published by Common Wealth described in detail how the retail market interacts with the wholesale market and transmission and distribution systems.[3] Regulations introduced in 2017 created a maximum “price cap” for what suppliers can charge to domestic consumers on default tariffs, following concerns raised by the Competition and Markets Authority (CMA) about a lack of effective price competition and low levels of consumer switching within the market.[4] The price cap is calculated on a quarterly basis by Ofgem based on wholesale, network, policy and other costs faced by suppliers.[5]

Notably, the price cap system still left consumers heavily exposed to the surge in wholesale prices in 2022, which was in turn driven by high natural gas prices. The cost to consumers was vast. Analysis by UCL estimated revenues to UK-based electricity generators in 2022 increased by almost £30 billion, compared to pre-pandemic levels.[6] Even before the 2022 surge, electricity prices faced by consumers had risen sharply over the previous decade, with the average electricity bill having increased by 36 per cent in real terms between 2010 and 2021 — compound annual growth of 2.8 per cent, compared to 0.3 per cent for average household disposable income (and 1.0 per cent for median).[7] The threat of even higher and more socially destructive prices led the Truss administration to introduce a temporary cap on prices born by consumers, with the Government footing the rest of the bill (estimated at £150 billion at the time), severely worsening its projected fiscal position just days before the doomed mini-budget.[8] The quarterly re-setting of the price cap based on forecasts also meant the rapid spike in wholesale prices were not immediately reflected in the prices charged to consumers, leading suppliers to make vast losses. This, along with a decade of lax regulatory oversight by Ofgem and poor financial resilience, led to a number of outright supplier failures at the cost of billions to consumers.[9]

Furthermore, as Dieter Helm has argued, the UK’s (internationally anomalous) decision to designate the task of smart meter rollout to retailers, rather than to distribution networks, has made the UK’s rollout much slower and more expensive than elsewhere.[10] This set-up has also granted retailers a lever with which to penalise customer switching (by preventing inter-operability of meters between different suppliers). Some retail suppliers have also undertaken morally-questionable behaviour through the forced installation of pre-payment meters on vulnerable customers.[11]

However, exposure to high wholesale price periods, poor regulation and questionable behaviour are far from the only challenges facing the retail market. Fundamentally, a profit-driven private retail market is being made redundant within the emerging power system based around mass low carbon low marginal cost generation, in which the state is increasingly playing an active role in fixing prices and (indirectly via the CfD and Capacity Market schemes) selecting the capacity mix. If the current wholesale market is a technological relic of an outdated and environmentally destructive way of distributing electrical power,[12] the current retail market must surely be an ideological relic of an outdated and socially destructive way of distributing economic power.

There are three main elements to this claim of anachronism in the supply market and thus the necessity of a public option for retail.

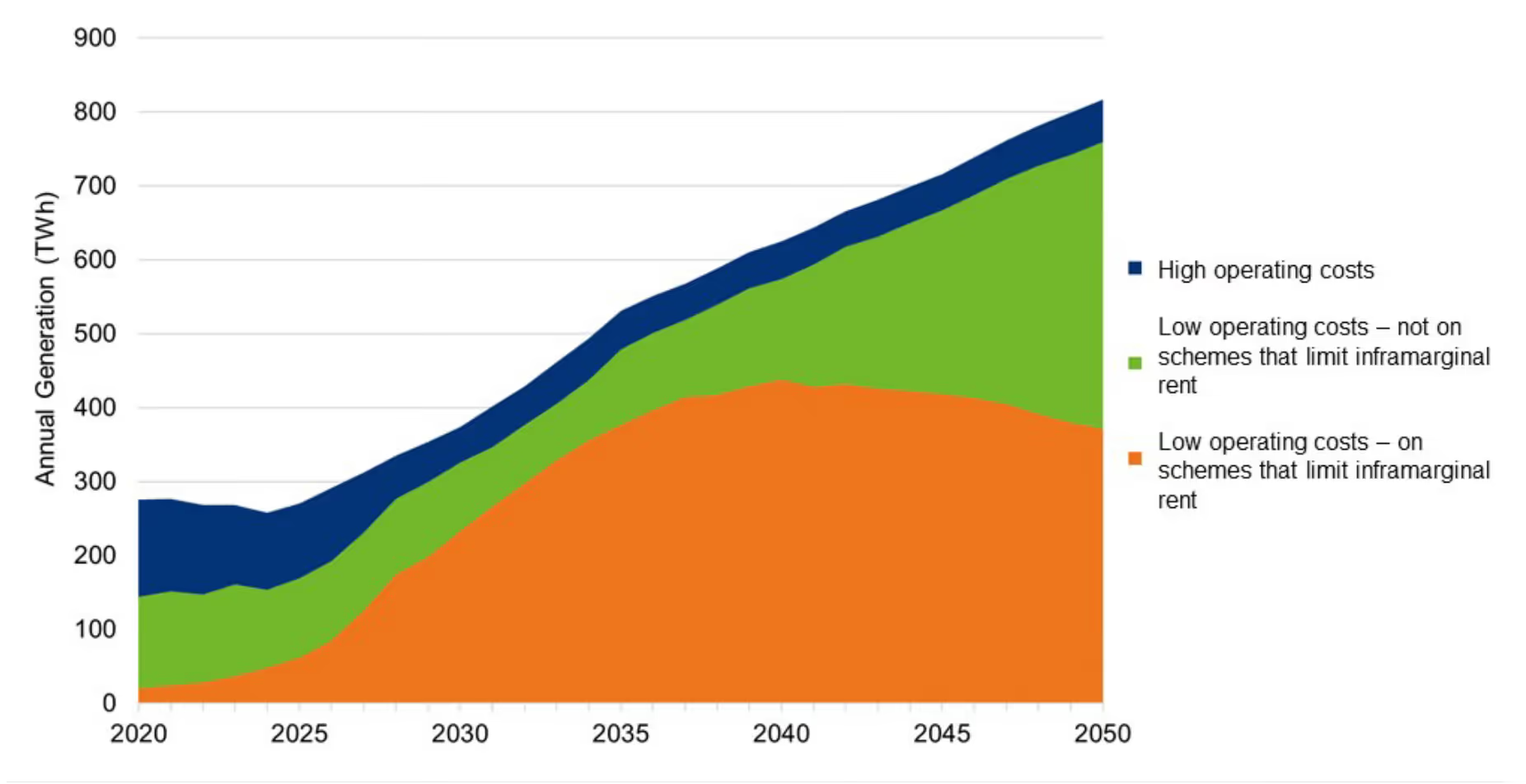

Firstly, as Dieter Helm has argued, the growing importance of ex ante fixed-price CfDs means new renewable generation capacity is already structurally bypassing retailers.[13] Under current policies, full power sector decarbonisation will render them functionally redundant — little more than outsourced debt-servicing companies with customer service relationships. Their role in price negotiation on behalf of consumers has in these cases been usurped by the state (with CfDs) or with large direct industrial users (PPAs), which has also narrowed the role they canonically played in hedging fossil price volatility in the interests of customers. For example, retail suppliers will tend to sign contracts with CfD-backed generators, but these contracts generally just specify a willingness to pay for units of power produced at whatever the reference price specified in the CfD contract (generally the Day Ahead wholesale price) happens to be at the time of generation. Difference payments equal to the gap between this time-varying reference price and a fixed strike price are made by the state-owned Low Carbon Contracts Company (LCCC). DESNZ analysis shows how significantly contracted generation of this type will come to dominate the generation mix.[14]

[.fig]Figure 1: Annual Generation by Contract Type, DESNZ Higher Demand Scenario[.fig]

[.notes]Source: DESNZ. Note: Figure shows: (i) technologies with high operating costs e.g. unbated gas, Power CCUS, Hydrogen to Power, (ii) technologies with low operating costs not on schemes that limit infra marginal rent, e.g. legacy nuclear, Renewable Obligation renewables, merchant renewables; (iii) technologies with low operating costs on schemes that limit infra marginal rent e.g. CfDs and nuclear RAB.[.notes]

This set up awkwardly preserves the spot market relationship between retailers and CfD generation assets, while neutralising the revenue variability to generators via LCCC payments after the fact. The LCCC then needs to finance this out of the Interim Levy Rate (ILR) on suppliers in the retail market. The ILR is backward-looking: it is set at a level that matches its aggregate revenues with the LCCC’s historic aggregate net CfD difference payments, and distributes the burden between retailers. This retrospective character means that, on the occasions that CfD generators are paying back to the LCCC thanks to elevated wholesale prices, the benefits of the lower strike price are not directly passed on to retailers until the ILR is lowered the following year. This can temporarily put retailers’ balance sheets under strain. In 2022, for example, retailers were paying exorbitant spot prices to both CfD and non-CfD generators, on top of a high ILR that reflected the LCCC’s higher net CfD payments in 2021. Only in 2023 would they be compensated in the form of a lower ILR.

[.fig][.fig-title]Figure 2: The CfD Strike Price is Financed by Interim Levy Rate on Retailers[.fig-title][.fig-subtitle]Net CfD payments vs ILR income, 2016-25 (£bn)[.fig-subtitle][.fig]

[.notes]Source: Common Wealth based on LCCC, as of July 2024.[.notes]

Passing on the benefits of below-market strike prices at the moment when consumers most need it is thus a liquidity strain on retailers. The day ahead reference price specified in the CfD contract also effectively forces CfD-backed intermittent generators to sell power at just this time horizon. As acknowledged in the Government’s own Review of Electricity Market Arrangement (REMA) this can be in tension with the desire among suppliers for longer term products, leading to a liquidity mismatch.[15]

There are signs that some incumbent suppliers recognise the coming redundancy of their existing business model, and are taking steps to address the problem. Most notably, Octopus Energy has become an important player in heat pumps, and in offering agile tariffs that reward consumer flexibility, as well as forcefully and publicly advocating for electricity market reform.[16] The emergence of the Demand Flexibility Service, in which consumers are paid to reduce their consumption during peak demand periods, also points to what the consumer interface could look like in a future system dominated by intermittent renewables.[17] However, more general proposals to radically and rapidly pivot suppliers' offerings in this direction, as suggested by the Energy Systems Catapult,[18] are belied by their poor performance in delivering the smart meter rollout, and overlook the fundamentally extractive and maladroit nature of much of the actually existing industry.

To the extent that supply companies are not yet redundant, their current fragmentation — and thus lack of monopsony power over the generation market (encouraged by policy) — has rendered them powerless to decouple the prices of gas and non-gas electricity.[19] This structural deficit needlessly amplified the gas shocks of 2022 into a full-blown energy crisis, raising the overall price of electricity above the level demanded by real resource constraints — with disastrous macroeconomic consequences still persisting today (including the prohibitively high interest rates now jeopardising renewable projects). Market-based reform options to "decouple" gas and electricity reviewed by the previous Government in REMA were eventually all dropped due to perceived complexity, and a view that continued reliance on the CfD scheme already reduces consumer exposure to high marginal price periods.[20] Although not noted as such, the previous Government’s own view[21] itself hints at the increasing redundancy of the retail market. However, REMA purposely did not include major proposals on reforms to the retail market or any attention to the potential role of public ownership or public investment in any part of the electricity system. In the long run, a publicly owned monopsony purchaser of power brings a greater level of coherence to the emerging pricing system, offering policymakers a flexible mechanism to manage prices and allocate costs progressively, without the need to set up a new "split" market. A retail arm of GB Energy which grows in scale over time while remaining financially secure, and which relates to generators and existing suppliers in the manner outlined below, is the most logical first step in achieving that coherence. Although complex, this approach is likely more politically feasible for the current Government, building on an existing manifesto policy, and would involve a much smaller initial capital outlay relative to immediately nationalising existing suppliers.

Finally, a competing cast of private profit-seeking retailers would, for obvious reasons, be unable to flexibly and autonomously implement the kind of progressive price discrimination to customers along the lines of the New Economics Foundation’s energy guarantee proposal,[22] Fuel Poverty Action’s Energy for All proposal,[23] or other variations of the “social tariff” proposal from groups such as National Energy Action.[24]

The only way to reconcile the profit imperative with the need to adequately serve “essential” customers with a given quantity of electricity at or below production cost (while conversely upholding the offsetting above-cost price premium for “luxury” uses of energy) would be through a cumbersome state-administered programme of credits that would similarly prompt the question of what purpose the retailers still serve, and why they should receive revenue from consumer electricity when they no longer serve any critical market coordination function. Such a social tariff or basic energy guarantee would be of great political importance in:

This points to clear opportunities for GB Energy, through a public retail arm, to engage with progressive price policies and to functionally restore coherence both within the retail sector and in relation to other parts of the energy system — both those being incorporated into GB Energy (including through the development of public options) and those remaining private.

A public retail arm of GB Energy should be structured as a company arm within the wider GB Energy institution. In this section we outline how the retail arm would relate to different types of generation and how it might build demand.

GB Energy ought to be investing in new generation capacity on the basis of system-level need, setting long term fixed prices for these assets ex post in order to recoup outturn costs, circumventing the CfD process which embeds ex ante cost uncertainties in order to derisk investments that are made on the basis of expected project-level profitability. Such an orientation to investment will preserve the volatility hedge offered by fixed-price PPAs, while removing “risk premium” to discrete projects and also allowing for cost/revenue redistribution among assets and thus leading to lower generation investment costs by GB Energy. Moreover, this relationship would bypass the wholesale private market and its marginal pricing system, which artificially inflates the cost of renewable energy by hooking it to the price of fossil fuels, thereby allowing clean, abundant energy to be sold at low cost.

The wholesale transaction with GB Energy’s retail arm would be an intersegment transfer for accounting purposes that also further reduces power prices, as there is no functional need to furnish retailers with a profit margin. Through this arm, households and businesses could directly purchase their electricity from GB Energy. Whilst their trading arrangements would be unique, generation assets owned by GB Energy and the GB Energy retail arm would still need to be participants in the Balancing Mechanism and ancillary markets, and to provide data and bids/offers to the system operator as normal. Further work would need to consider the nature of different arms of GB Energy’s exposure to imbalance pricing, and any adaptations needed to industry codes and trading platforms to accommodate this set up.

A GB Energy retail arm that takes over the function of the LCCC as the CfD counterparty for new contracts would gradually render the ILR system redundant. This would simplify and speed up the means for returning wholesale revenues in excess of the strike price to consumers. Where payments need to be made to or from generators, these should be funded progressively within GB Energy’s consumers bills (respecting the wider social tariff/NEG), with additional payments coming from general taxation where needed. This would be distributionally much fairer than the current system of levy-funded payments, and help improve incentives for electrification of domestic heating and vehicles. Reducing responsibility from LCCC for managing power CfDs would also allow it to focus more on its new responsibilities as the counterparty for contracts in others sectors such as CCUS, Hydrogen and Greenhouse Gas Removals.

Once it has sufficient consumer demand, GB Energy retail could use monopsony purchasing power to keep the wholesale price of non-CfD electricity as close to actual average cost as feasible. For non-dispatchable sources this could be arranged through PPAs that are based on historic costs, ongoing and projected finance costs, and a reasonable assessment of operation and maintenance costs (which are a small proportion of LCOE for wind and solar). For example, such arrangements could be made for operational renewable assets coming to the end of Renewable Obligation contracts, or privately owned “repowered” assets (as an alternative to lumping these projects into an already overburdened CfD scheme). Cost transparency on the part of generators should be mandated to this end. And informational asymmetries (of the kind that bedevil Ofgem’s relationship with transmission and distribution companies) should be tackled as a matter of policy urgency.

The retail arm could also be a key participant in small-scale renewables (both public assets, such as community projects supported by the Local Power Plan, and private) by purchasing exported electricity from rooftop solar and other technologies under the terms of the Smart Export Guarantee (SEG). SEG tariffs offered by incumbent retailers are often quite low and complex (tariffs actually declined year on year in the most recent data) with more generous tariffs frequently being “bundled” with requirements to purchase imported power or equipment from the same company.[25] Government research has shown awareness of the SEG is low and upfront costs are a major barrier to installation of rooftop solar.[26] A GB Energy retail arm should seek to offer the most open and generous export tariff available, advertise this, and coordinate with Distribution Network Operators to identify creative ways of managing and using surplus generation from small scale projects. This could include aggregation of small-scale assets to monetise their system value, analogous to the Virtual Power Plants model recently advocated by the Centre for Public Enterprise in the United States.[27]

A key question is how a GB Energy retail arm could build sufficient consumer demand to perform the offtake functions outlined above, and longer term to become a monopsony purchaser within a vertically integrated publicly owned power system. To begin with, it would benefit from strong brand recognition and the ability to price tariffs in a more equitable way, attracting a section of consumers organically. Polling commissioned by Common Wealth has shown that, given the option to switch from their current energy supplier to a publicly owned energy company, a third of the public would choose to switch whereas only around a quarter would choose to stay with their current supplier. In the medium term, serious thought should be given to the retail arm taking on “supplier of last resort” functions for failed suppliers, and a natural home for suppliers entering into special administrative regimes. It could also be the default or preferred supplier for public sector organisations like schools, hospitals and Government departments. Attracting private sector commercial and industrial customers could be developed in tandem with wider government policy on industrial strategy, and a developed system for the state enabling progressive PPAs (analogous to the Green Power Pool option abandoned in REMA).[28] Longer term, thought should be given to a reformed role for existing supply companies in performing some of the GB Energy retail arm’s functions (such as tariff design, metering and customer service) as competitively tendering contractors, in exchange for their customers.

Setting up a public option retail arm would require significant reform of regulations and potentially legislative changes beyond what is likely to be in scope of the upcoming Great British Energy Bill. A consultation period would be needed to consider how best to do this. We would advocate the new Government publicly announcing plans to consult on this soon, with a view for the retail arm to be operational prior to the next general election.

There are no doubt risks associated with what we have proposed here. Lessons need to be learned from the Robin Hood Energy company set up by Nottingham City Council that ultimately failed, causing political damage and millions of pounds of losses.[29] The capabilities and borrowing ability of national government relative to a single local authority should help. An ineffective retail arm that consumers dislike could also hurt the GB Energy brand. To avoid this, high-quality customer service would need to be a high priority.

Importantly, the risks of inaction, of allowing the energy market to fragment further, and of underdelivering on what voters expected from GB Energy are also large. The Government would do well to start looking at a public option retail arm of GB Energy now.

[1] 19 per cent of 2,032 respondents selected this as their most preferred description of GB Energy. 36 per cent of 1,447 respondents selected this as an additional function they would like GB Energy to fulfil. Respondents could not select their most preferred description as an additional function. Respondents who selected "Don’t Know" or "None of These" for their most preferred description were not asked about additional functions they would like to see.

[2] Sandy Brian Hager, Joseph Baines and Miriam Brett, ”Power Ahead: An Energy System Fit For The Future”, Common Wealth, 2022. Available here. Note that this figure relates to British Gas, EDF Energy, E.ON, Npower, Scottish Power and SSE, whose combined market share was close to 100 per cent at the start of the 2010s. New entrants, the sale of Npower to E.ON, and since 2021 the moving of customers from failed suppliers, have changed relative market positions considerably, with Octopus Energy now one of the largest providers. See “Retail Market Indicators”, Ofgem, [undated]. Available here.

[3] Explainer: How Britain’s Energy System Works — and Why It Needs an Overhaul”, Common Wealth, 2023. Available here.

[4] “Energy Market Investigation”, Competition and Markets Authority, 2016. Available here.

[5] “Energy price cap”, Ofgem, [undated]. Available here.

[6] Serguey Maximov, Paul Drummond, Philip McNally, Michael Grubb, “Where does the money go?”, UCL Institute for Sustainable Resources , 2023. Available here.

[7] Paul Bolton, “Domestic energy prices”, House of Commons Library, 2024. Available here.

[8] George Parker, Jim Pickard and Chris Giles, “Liz Truss unveils £150bn UK energy plan but limits business support to six months” , Financial Times, 2022. Available here.

[9] An independent report commissioned by Ofgem found significant fault with the regulatory approach aimed at promoting competition, noting it “does not seem to have been justified by an evidence based assessment of trade-offs or a detailed understanding of the supplier business models and supplier incentives” and that this led to weak financial resilience running into the energy crisis. “Review of Ofgem's regulation of the energy supply market”, Oxera, 2022. Available here.

[10] Dieter Helm, “Energy network regulation failures and net zero”, 2023. Available here.

[11] Kevin Peachey, “Compensation paid for force-fitting of prepayment meter”, BBC News, 3/4/2024. Available here.

[12] Donal Brown, Chris Hayes, Mathew Lawrence, Adrienne Buller. “A Wholesale Transformation: Evaluating Proposals for Electricity Market Reform”, Common Wealth, 2023. Available here.

[13] Dieter Helm, “Luck is not an energy policy – the cost of energy, the price cap and what to do about it”, 2021. Available here.

[14] “Review of electricity market arrangements (REMA): second consultation”, p.35, Department for Energy Security and Net Zero, 2024. Available here.

[15] Ibid, pp.109-11.

[16] Leo Hickam, Simon Evans, “The Carbon Brief Interview: Octopus Energy’s Greg Jackson”, Carbon Brief, 13/5/2024. Available here.

[17] “Demand Flexibility Service (DFS)”, National Grid ESO, [undated]. Available here.

[18] “Clean Energy Retail”, Energy Systems Catapult, 2022. Available here.

[19] Brown et al., “A Wholesale Transformation”, Common Wealth. Available here.

[20] “Review of electricity market arrangements (REMA): second consultation”, pp.35-38, Department for Energy Security and Net Zero, 2024. Available here.

[21] Ibid.

[22] Alex Chapman, Chaitanya Kumar, “The National Energy Guarantee”, New Economics Foundation, 2023. Available here. This proposal would guarantee a volume of free or low cost essential energywith higher per unit costs for tiers of consumption above this.

[23] “Manifesto”, Energy For All, [undated]. Available here.

[24] “Social Tariff Letter”, National Energy Action, 2023. Available here. Broadly, a social tariff involves targeted support, in the form of cheaper tariffs, to vulnerable or fuel poor households.

[25] “Smart Export Guarantee (SEG) Annual Report 2022-23”, Ofgem, 2023. Available here.

[26] “Adoption of rooftop solar photovoltaic panels in the UK”, Department for Business Energy and Industrial Strategy, 2021. Available here.

[27] Yakov Feygin, “Virtual Power Plants: Financing a Distributed Energy System”, Center for Public Enterprise, 2024. Available here.

[28] Michael Grubb, Paul Drummond and Serguey Maximov, ”Separating electricity from gas prices through Green Power Pools: Design options and evolution”, UCL Institiute for Sustainable Resources, 2022. Available here.

[29] David Pittam, ”Robin Hood Energy: The failed council firm that cost city millions”, BBC News. Available here.